Imagine this scene. You are standing in front of a bungalow you always pictured living in. You check your account balance and your heart sinks. A past bankruptcy flashes in your memory, and you tell yourself the dream is over.

Many people wonder how to get a mortgage after bankruptcy, thinking it might be impossible. The truth is different. With the right planning, clear steps, and steady financial rebuilding, bankruptcy changes the starting line, not the finish line. Owning a home is still possible if you know what to do next.

How to Get a Mortgage After Bankruptcy in Canada

Short answer: bankruptcy is a setback but not the end of your homeownership dream. With a clear plan, patient rebuilding, and the right help, many people get a mortgage again within a few years. This guide gives a step by step plan, lender realities, practical tips, and ready to use templates so you can move forward with confidence.

The Impact of Bankruptcy on Your Mortgage Eligibility

Think bankruptcy ends your homeownership dreams? The reality is different. Understanding how it affects your mortgage eligibility is the first step to getting back on track.

What bankruptcy means in Canada

Bankruptcy is a legal process that helps people clear or reorganize overwhelming unsecured debt. It gives a fresh start but also appears on your credit records. That record tells lenders about a severe credit event in your past and affects how they view your risk.

In Canada, a bankruptcy typically stays on credit reports for six years after the discharge date, though in some provinces TransUnion may report it for seven years. Repeated bankruptcies can remain for much longer.

Credit score effects

Bankruptcy usually causes a large drop in credit score. But the score is not static. It can improve steadily if you rebuild responsibly. Payment history and recent good behaviour matter more to lenders than a single old event once you have demonstrated months and years of consistent payments.

Lender perspective

Lenders view bankruptcy as a strong negative signal. Their decisions are driven by risk management. Some need long windows of rebuilt credit and clean behaviour. Others will consider your whole story if you can show stable income, savings, and reliable recent payments.

Bankruptcy versus consumer proposals

A consumer proposal is an alternative insolvency process where you negotiate to pay a portion of debts over time. It also affects credit reports differently and can sometimes be seen as less severe than bankruptcy by certain lenders. The exact impact depends on the lender and the specifics of the file.

Waiting periods overview

There are no universal rules. Lenders have different risk appetites and criteria. The type of lender you approach determines the likely waiting period before a mortgage is realistic. Concrete timelines are discussed next.

Waiting Periods by Lender Type

Not all lenders treat bankruptcy the same. Knowing the typical waiting periods for different lender types can help you plan your next steps and get back into the housing market sooner.

Prime or traditional lenders

Large banks and credit unions typically need more evidence of rebuilding. A common benchmark for many prime lenders is about two years after discharge, combined with established credit activity and on time payments. This is a general rule and individual cases vary.

Alternative or B lenders

B lenders or alternative lenders consider more than just your credit score. They look at your current income, down payment, and the full story. They may consider cases starting as early as a few months after discharge, though more commonly three to twelve months is quoted depending on the case and collateral. These options are more expensive but faster.

Private lenders

Private lenders are the most flexible. They can fund deals quickly, sometimes immediately after discharge. The tradeoff is much higher interest rates, larger fees, and short term focus. Private lending is usually a bridge strategy not a long term solution.

Practical note

Timelines vary widely by case. Documentation, steady income, a decent down payment, and a clear explanation of the bankruptcy will all shorten the path. Always document everything and focus on recent positive behaviour.

Can You Really Get a Mortgage After Bankruptcy?

Short answer: yes, under conditions.

Key factors lenders evaluate

Lenders typically look at these items in a file after bankruptcy:

- Time since discharge.

- Rebuilt credit history with timely payments.

- Steady income and employment stability.

- Size of down payment and available assets.

- Debt to income ratio and current liabilities.

- Source of down payment and whether funds are documented.

Why private and alternative lenders may be more flexible

B lenders and private lenders are willing to accept more risk in exchange for higher returns. They will consider the whole story: maybe you had a business failure, medical bills, or a one time shock. They will weigh recent steady payments heavily. The tradeoff is cost and potentially shorter amortization or higher required equity.

Realistic expectations

Early on you will likely face higher interest rates and stricter conditions. Over time, with good credit behaviour and savings, you can refinance to a better mortgage. Think of early financing as stepping on a ladder rung. You will climb down to lower cost as your profile improves.

Must Check: Mortgage Broker vs Real Estate Agent

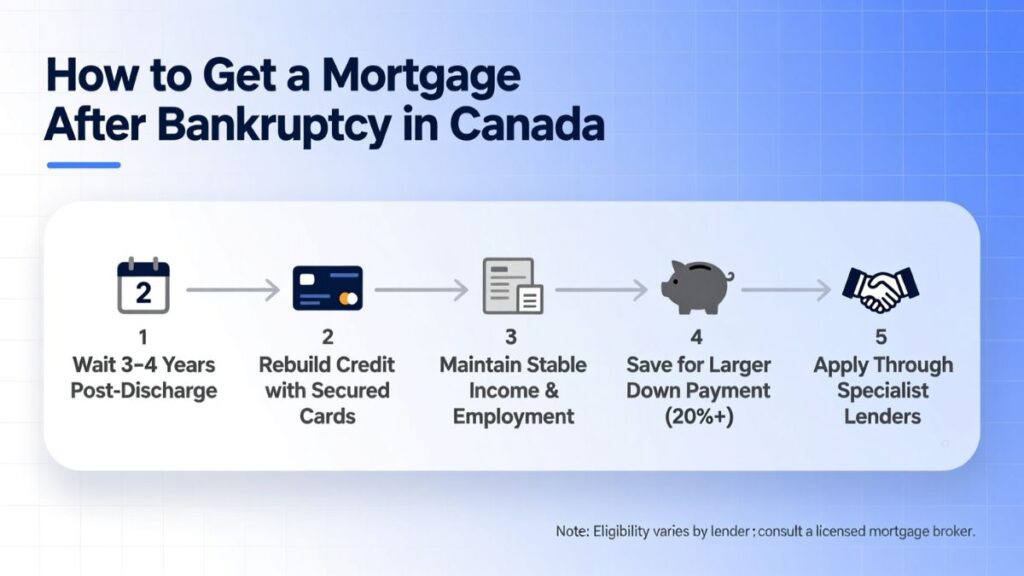

A Step by Step Action Plan to Rebuild Your Financial Profile

Here is a practical roadmap you can follow. Treat it like a project with milestones.

Step 1: Fresh start credit check

Get your full credit reports from Equifax and TransUnion as soon as you are discharged. Check for mistakes and disputes. An accurate starting point helps you track progress.

Why this matters: errors are common and correcting them can boost your score quickly. Government guidance confirms the timeline and encourages checking reports.

Step 2: Reestablish credit strategically

Follow the rule of two. Aim to responsibly hold two new credit accounts within the first year. Practical choices:

- A secured credit card with a low limit tied to a deposit.

- A small credit builder loan from a bank or credit union.

Use them, then pay them in full each month. This creates a fresh, positive payment history.

What secured cards and credit builder loans do

- Secured card: you put down a deposit that sets your limit. Use it for small purchases and pay monthly.

- Credit builder loan: the bank holds the loan funds in a savings account while you pay. When you complete the loan the funds are released to you and your positive payments are reported.

Step 3: Build a positive payment record

Pay every bill on time. Payment history is the single most important driver of credit score recovery and a strong predictor of future loan performance. Experts and credit models consistently show payment history is a top factor.

Keep credit utilization low. Aim to use less than 30 percent of available credit on any revolving account. Low utilization plus perfect payments equals steady recovery.

Step 4: Save for a larger down payment

A larger down payment reduces lender risk and opens more lender doors. Targets:

- Aim for 10 percent to 20 percent if possible.

- 20 percent is a strong benchmark because it reduces loan to value risks and eliminates mortgage insurance in many standard cases.

Practical ways to save:

- Dedicated high interest savings plan.

- Use the RRSP Home Buyers Plan if eligible. The HBP limit was increased to 60,000 for qualifying withdrawals in recent years. That can be a major boost for a down payment.

- Gifts from family with clear documentation.

- Side income dedicated to down payment.

Step 5: Manage behaviour

Avoid new unnecessary debt and avoid multiple hard credit inquiries. Keep steady employment. Lenders want to see stability and discipline.

Saving for a Down Payment

A bigger down payment can open doors even after bankruptcy. Saving strategically not only lowers lender risk but also boosts your chances of getting approved faster.

Why a larger down payment matters

A bigger down payment lowers the loan to value ratio which is closely linked to default risk in mortgage research. Lenders charge lower interest when they see more borrower equity because recovery costs in default are lower. Studies show down payment size reduces delinquency risk.

Target amounts

- 10 percent gives much better odds than zero.

- 20 percent is a strong target and often unlocks better mortgage terms.

- For modest budgets, even 5 percent plus strong compensating factors can work with alternative lenders.

Ways to save

- Open a dedicated savings account and automate transfers.

- Set a monthly budget that cuts discretionary spending.

- Consider RRSP HBP withdrawals up to 60,000 when eligible. Make sure you understand repayment rules.

- Ask the family for gift funds with a letter documenting the gift.

How down payment offsets past credit issues

A large down payment is proof of discipline and financial ability. For a lender, someone who can save 20 percent shows current stability even with an older bankruptcy. It reduces the lender’s exposure and can shorten waiting periods or improve terms.

Exploring Your Mortgage Options After Bankruptcy

Not all lenders see bankruptcy the same way. Exploring your mortgage options after bankruptcy helps you find the right path to approval without unnecessary delays or high costs.

Prime lenders

Banks and credit unions offer the lowest rates but strict criteria. They will typically want evidence of several years of clean credit behaviour, steady employment, and often 20 percent down or strong compensating factors. This is the goal for long term affordability.

Alternative or B lenders

B lenders are more flexible about credit score and past events. They look at the full picture: income, equity, and current payment history. They often offer two to three year term mortgages that let you improve your profile and then refinance to a prime lender. Expect higher rates and stricter amortization rules.

Private lenders

Private lending is fast and flexible. Expect higher cost and shorter terms. Good for urgent purchases, renovations, or when you need a short bridge loan. Use cautiously and with a clear exit or refinance plan.

Comparing rates and fees

Do not just compare the quoted rate. Total cost matters. Look at:

- Rate and amortization length.

- Fees and penalty structures.

- Prepayment rules.

- Whether the mortgage is insured and the cost of mortgage insurance.

When to choose each option

- Choose prime banks when you have clean rebuilt credit and lower risk.

- Choose B lenders when you need access sooner but can accept higher cost temporarily.

- Choose private lenders only for short term needs with a clear plan to refinance.

The Role of a Mortgage Broker

A mortgage broker can be your guide after bankruptcy. They know which lenders will consider your full story and how to present your file for the best chance of approval.

How brokers help

A broker shops your file to multiple lenders and can match your case to the lender most likely to approve you. They package documents and present your story in a way underwriters understand.

Specialty brokers

Look for brokers experienced in post bankruptcy and bad credit cases. They know which lenders consider the full story and which need long waiting periods.

Tailored strategies

A broker can advise on timing, recommended down payment, and which compensating factors lenders will value most. Brokers also help you avoid costly lender traps and long term bad deals.

Local advantage and AJP Mortgage

Local market knowledge matters. A broker based where you are working and buying understands local appraisal and market realities. For personalized help in the Brampton area, a local expert such as AJP Mortgage can review your file, recommend a tailored plan, and connect you with lenders who take your situation seriously.

The Mortgage Application: What to Expect

The mortgage application process can feel overwhelming after bankruptcy. Knowing what to expect and preparing the right documents can make approval smoother and faster.

Required documents

Prepare these early:

- Notice of discharge from bankruptcy.

- Full credit report copies from Equifax and TransUnion.

- Employment letter and recent pay stubs.

- T4s and tax returns if self employed.

- Bank statements showing savings and down payment source.

- ID and proof of address.

- Gift letter if down payment is a gift.

Letter of explanation

Write an honest concise letter explaining the bankruptcy cause and what changed. Focus on facts, your timeline, and the steps you took to recover. Lenders prefer clear transparency plus proof that the issue was not repeated.

Preapproval importance

A preapproval tells you realistic borrowing power and strengthens offers to sellers. It also reveals income documentation gaps before you find a property.

Underwriting process

Underwriting checks employment, income continuity, credit report, the source of down payment, and sometimes rental history or references. Underwriters look for consistency and proof that the risk is reduced.

Pro Tips to Improve Your Chances of Approval

Small actions can make a big difference. These pro tips will help you improve your chances of mortgage approval even after bankruptcy.

- Show steady income: stable employment or documented self employment with at least two years of steady earnings where possible.

- Lower debt to income ratio: pay down consumer debts where possible before applying.

- Demonstrate savings discipline: regular deposits into savings show future reliability.

- Limit credit inquiries: many enquiries reduce lender confidence.

- Use compensating factors: large down payment, co borrower with good credit, or long employment history can help.

- Consider a shorter amortization initially to reduce payment strain and risk.

Common Mistakes to Avoid

Avoiding these mistakes can make getting a mortgage after bankruptcy easier:

- Applying too soon: Lenders need to see that you’ve rebuilt your credit. Waiting a bit helps your chances.

- Not checking your credit report: Mistakes happen. Make sure your report is correct.

- Taking on new debt or big purchases Extra debt makes lenders nervous. Keep your spending steady.

- Borrowing more than you can afford: Only take what you can comfortably pay.

- Using expensive private lenders without a plan: Private lenders are fast but costly. Have a plan to switch to a cheaper lender later.

Follow these tips and your path to homeownership will be smoother.

Realistic Timeline: How Long Before You Can Buy Again?

Typical timelines to keep in mind:

- Prime lenders: commonly about two years after discharge with rebuilt credit and stable income. Some cases require longer.

- Alternative or B lenders: sometimes consider you between three and twelve months after discharge depending on evidence of recovery and down payment.

- Private lenders: immediate in many cases but at much higher cost.

Why patience helps

Waiting and rebuilding gives you access to better rates, more lender choices, and lower lifetime cost. Rebuilding credit and savings turns the story from a risk to an opportunity.

Short success stories

- A buyer who saved a 20 percent down payment and made two years of perfect payments qualified with a credit union and later refinanced to a bank.

- A self employed borrower who used a B lender mortgage for one year, improved cash flow, then moved to a prime lender for a better rate.

Conclusion

Bankruptcy changes the map but not the destination. Wait as needed, rebuild credit with disciplined steps, save a meaningful down payment, choose the right lender, and work with a specialist.

Bankruptcy is a setback not an end. People rebuild. With a plan, discipline, and the right help, homeownership becomes achievable again.

If you want a personal review and a step by step plan tailored to your situation, contact AJP Mortgage. We can review your file, outline timelines, and connect you to lenders who will listen to your story.

Appendix

Sample letter of explanation template

Use this as a starting point and adapt details to your case.

[Date]

To whom it may concern

Subject: Letter of explanation regarding bankruptcy

I, [Your full name], was discharged from bankruptcy on [date]. The bankruptcy was filed due to [brief reason e.g. medical bills, business failure, job loss]. Since discharge I have taken the following steps to rebuild my finances:

- Obtained fresh credit reports from Equifax and TransUnion and corrected inaccuracies.

- Opened and responsibly used a secured credit card and a small credit builder loan, with all payments made on time.

- Saved for a down payment of [amount] with documented bank statements.

- Maintained steady employment at [employer name] since [date] with current monthly income of [amount].

- Completed financial counselling on [date] and adopted a monthly budget and emergency savings plan.

I am seeking mortgage financing for the purchase of [property details]. I can provide full documentation of my employment, bank statements, proof of down payment source, and character references on request.

Thank you for considering my application.

Sincerely

[Name]

[Contact details]

Document Checklist Before Applying

Getting your documents ready early makes the mortgage process smoother. This checklist shows exactly what you need before applying after bankruptcy.

- Notice of discharge

- Equifax and TransUnion credit reports

- Employment letter and pay stubs

- T4s and tax returns for last two years

- Bank statements for last three months

- Proof of down payment source and gift letter if applicable

- ID and address proof

Quick comparison: Prime versus B lenders versus private lenders

Not all lenders are the same. This quick comparison of prime, B, and private lenders shows the pros, cons, and what to expect after bankruptcy.

| Lender Type | Pros | Cons |

| Prime Lenders | Lowest rates, long-term affordability | Stricter rules, longer waiting periods |

| B Lenders | More flexible underwriting, consider full story | Higher rates, often shorter terms |

| Private Lenders | Fastest, most flexible | Highest cost, fees, short-term focus |

Final practical checklist to get started today!

Ready to take action? This practical checklist helps you start rebuilding your finances and move closer to getting a mortgage after bankruptcy.

- Order credit reports from Equifax and TransUnion.

- Write your letter of explanation draft.

- Open one secured credit card and one credit builder account.

- Start a dedicated down payment savings plan and automate transfers.

- Contact a mortgage broker experienced in post bankruptcy cases such as AJP Mortgage for a personalized plan.

Sources and further reading

Key references used for timelines and guidance:

- Government of Canada guidance on how long bankruptcy appears on credit reports. Canada.ca

- Canada Revenue Agency information on the Home Buyers Plan and withdrawal limits. Canada.ca

- Consumer credit and payment history importance from myFICO and Urban Institute research on payment history as a predictor of mortgage performance. myFICO+1

- Practical timelines and guidance from consumer mortgage advisors and firms. Hoyes, Michalos & Associates Inc.+1

- Explanation of alternative B lenders and how they operate. True North Mortgage

- Research on down payment and default risk and how equity affects mortgage performance. HUD User