Buying a home in Ontario is hard. It’s not the monthly payments that worry most people. It’s saving up for the down payment. With home prices going up, even saving 5 percent can feel impossible.

So, how to buy a house in Ontario with no down payment? It might sound too good to be true, but it’s not. There are real ways to do this if you know where to look.

Whether this is your first home, you’re new to Canada, or the market feels out of reach, no money down mortgage options in Ontario might be your way in.

At AJP Mortgage, we’ve helped many people find ways to get into a home faster. This guide will explain how zero down mortgages work, the options you have, the risks, and how to get approved.

By the end, you’ll understand how to buy a home with no down payment and why having the right mortgage broker can help you every step of the way.

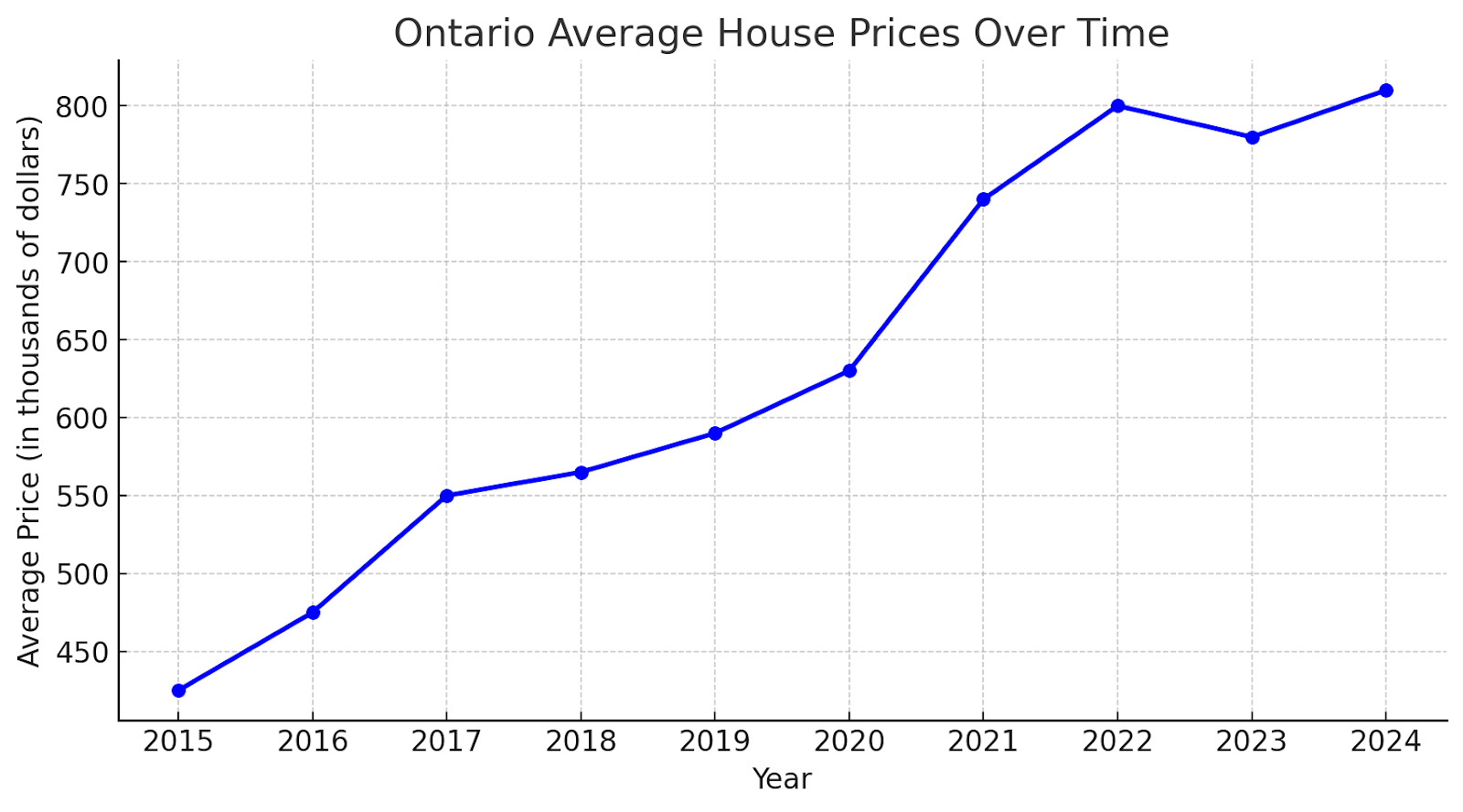

From the above graphs we can have an idea that why people care more about House mortgage rates Ontario.

What is a No Down Payment Mortgage?

A no down payment mortgage in Ontario means you don’t have to put any money from your own savings when buying a home. Instead, the full purchase price is covered by a mix of a regular mortgage and other financing sources.

In Canada, lenders are required by law to limit the mortgage amount to 95 percent of the home’s price when it’s an insured mortgage.

This means you usually can’t get 100 percent financing with just one mortgage product. But there are ways to get a 0 down mortgage in Ontario by combining your main mortgage with other options like:

When you put these together the right way, you can buy a house with no down payment. Many Ontario homebuyers use these strategies to get into the market faster.

Why Banks No Longer Advertise “Zero Down”

Before 2008, some Canadian lenders offered 100 percent financing, often called zero down mortgages, and they promoted them widely. But after changes to federal mortgage rules, these products were taken off the market.

That doesn’t mean you can’t buy a home with no money down mortgage Ontario options today. It just means you need a smart, legal plan to make it work. An experienced mortgage broker can create this plan easier than going straight to a bank.

If you’re wondering how to buy a house in Ontario with no down payment and want help from the best mortgage broker in Ontario or the best mortgage broker in Mississauga, you need someone who knows both the traditional lending rules and alternative financing options.

At AJP Mortgage, this is exactly what we do every day.

How No Down Payment Mortgages Work in Ontario

Getting a no down payment mortgage in Ontario is not about finding one single product. It’s about putting together a smart financing plan that meets lender rules and covers your upfront costs.

Here’s how it usually works

Main Mortgage Approval (Up to 95% of Purchase Price)

Your main mortgage usually covers up to 95 percent of the home’s price. This part follows regular mortgage rules, which means you still need to pass the lender’s stress test, prove steady income, and have a good credit score.

Finding the Remaining 5%

The rest of the money for your down payment comes from another approved source. Common options include:

A skilled mortgage broker will help you find the right mix that fits your budget and the lender’s rules. This is how many people buy a house with no down payment in Ontario today.

Covering Closing Costs

Remember, no down payment mortgage doesn’t mean no money at all. You still need to cover closing costs like legal fees, land transfer taxes, and appraisal costs.

In Ontario, these can add up to 1.5 to 4 percent of the purchase price depending on where the home is and what type it is.

The Broker Advantage

Banks usually don’t offer this kind of financing directly. They stick to their own products, which means if you don’t have a down payment saved, you might hit a dead end.

That’s where a mortgage broker comes in. Brokers work with many lenders, including ones that accept gifted funds, personal loans, or blended financing. This makes it possible to get a no money down mortgage Ontario without waiting years to save.

Whether you want the best mortgage broker in Ontario or the best mortgage broker in Mississauga, working with the right professional can be the difference between buying now or waiting years.

Who Can Get a No Down Payment Mortgage in Ontario?

Not everyone can get a no down payment mortgage in Ontario. Lenders see these loans as risky, so they have stricter rules. But if you plan well and work with the right mortgage broker, you can still qualify.

Good Credit Score

Lenders usually want your credit score to be around 650 to 680 or higher. The better your score, the easier it is to get approved and get a better rate. If your score is low, a broker can help you improve it.

Stable Income

You need to show steady income with pay stubs, tax forms, or other proof. If you’re self-employed, you may need to show extra documents like bank statements.

Manageable Debt

Lenders want to see that your monthly debts are not too high compared to your income. Usually, your total debts should be less than 40 to 44 percent of your monthly income.

Proof of Down Payment Source

Even if you’re not using your own money, lenders want to know where the down payment money is coming from. This can be:

Closing Costs Need Your Own Money

While you can borrow for the down payment, you still need your own money for closing costs. You should have about 1.5 to 4 percent of the home price saved for things like legal fees and taxes.

A good mortgage broker can help you put together your application and connect you with lenders who offer no down payment mortgages.

Whether you want the best mortgage broker in Ontario or in Mississauga, working with a pro makes a big difference.

Pros and Cons of a No Down Payment Mortgage

Like any mortgage, choosing a no down payment mortgage in Ontario has good points and some drawbacks. Knowing both sides will help you decide if it’s right for you.

The Good Stuff

Thinking about a no down payment mortgage? Before you jump in, let’s weigh the hidden perks and pitfalls so you know if it’s really the good stuff.

Get Into the Market Faster

Instead of saving for years, you can buy a home sooner. This is great when house prices keep going up faster than you can save.

Keep Your Savings Safe

You don’t have to use up your emergency money or investments to get a home. You can keep that money for things like fixing up your new place or unexpected costs.

Build Credit and Equity Sooner

Owning a home and paying your mortgage on time can improve your credit score. Plus, you start owning part of your home right away, which helps if you want to refinance or borrow later.

Lock In Today’s Interest Rates

If rates are going up, buying now can save you money compared to waiting until you save enough for a traditional down payment.

The Not-So-Good Stuff

Not all that glitters is gold. Let’s uncover the not-so-good stuff about no down payment mortgages before they catch you off guard.

Monthly Payments Are Higher

Because you borrow more money, your monthly mortgage payments will be bigger. This can make your budget tighter.

You Pay More Interest Over Time

Borrowing the full price means paying more interest during the life of the loan.

Harder to Qualify

Lenders are careful with zero down loans. You might need a better credit score and less debt to get approved.

Risk if Home Values Drop

If the housing market falls, you might owe more than your home is worth. This is called being underwater on your mortgage.

Pro Tip: A good mortgage broker can help you avoid some of these risks. They can find better rates, make sure your payments are manageable, and help you find the best plan for your future.

How to Buy a House in Ontario with No Down Payment

Buying a home with no down payment in Ontario might seem tricky at first. But if you follow a clear plan, it becomes much easier. Here’s a step-by-step guide to help you get a no down payment mortgage Ontario that fits your needs.

Step 1: Check Your Financial Health

Before you apply, check your credit score and debts. Most lenders want a credit score of 650 or higher for zero down mortgages. If your score is low, work on improving it. Also, try to pay off high-interest debts to lower your debt-to-income ratio.

Step 2: Gather Your Documents

Get your proof of income ready. This can be recent pay stubs, T4 slips, or tax returns if you’re self-employed. Also, gather any documents that prove gifted funds or lines of credit you plan to use for the down payment.

Step 3: Work with a Good Mortgage Broker

Finding the right lender for a no money down mortgage Ontario isn’t always easy. A mortgage broker like AJP Mortgage knows the market and can connect you with lenders offering zero down mortgages Ontario. They can help find programs that fit your situation.

Step 4: Explore No Down Payment Options

Ask your broker about choices like:

Zero down payment mortgage programs from lenders or government incentives

Gifted down payment letters from family

Rent to own Ontario no down payment plans

Personal loans or lines of credit to cover your down payment

Step 5: Get Pre-Approved

Get pre-approved for a mortgage that includes your zero down mortgage loans plan. This shows sellers you’re serious and gives you a clear budget to shop with.

Step 6: Shop for Your Home

Look for homes within your budget. Think about location, size, and condition. Don’t forget about extra costs like closing fees and property taxes.

Step 7: Make Your Offer

With your pre-approval and down payment plan ready, you can make an offer with confidence. Sellers like buyers who are prepared and can close quickly.

Step 8: Finalize Financing and Close

Your mortgage broker will help finalize everything with the lender, including any loans or credit lines you’re using for the down payment. Once approved, you’ll close on your home and start owning it without a traditional down payment.

Pro Tip: Don’t forget about closing costs. Even with a 0 down mortgage, you need savings for legal fees, land transfer taxes, and other upfront costs. Plan for about 1.5 to 4 percent of the home’s price to cover these.

No Down Payment Mortgage Programs Available in Ontario

If you’re wondering how to buy a house with no down payment in Ontario, it helps to know what programs are out there. These options make zero down payment mortgages possible for many buyers who don’t have a big lump sum saved up.

First-Time Home Buyer Incentive (FTHBI)

This program from the Canadian government offers 5 to 10 percent of the home’s price as a shared equity mortgage. It lowers your monthly mortgage payments and cuts down the cash you need at closing.

For first-time buyers only

Helps reduce upfront cash needed

You’ll repay the government’s share when you sell or after 25 years

Home Buyers’ Plan (HBP)

HBP lets you take out up to $35,000 from your RRSP to use for your down payment. It’s a tax-free loan you pay back over 15 years.

Can be combined with other mortgage options

Great for buyers with RRSP savings

Gifted Down Payment Programs

Many lenders accept down payments given by family members. You just need a clear gift letter saying you don’t have to pay the money back.

Helps many buyers with no money down mortgages

Common for first-time buyers getting help from family

Rent to Own Ontario No Down Payment Options

With rent-to-own, you rent a home with the chance to buy it later. Part of your rent goes toward the down payment.

Helps people without savings start owning a home

Can act as an alternative to a no down payment mortgage

Terms vary, so ask a mortgage expert for help

Lender-Specific Zero Down Mortgage Programs

Some credit unions and private lenders offer zero down mortgage programs. These may include:

Personal loans or lines of credit to cover the down payment

Easier qualification if you have strong credit

Higher interest rates or mortgage insurance to cover lender risk

You May Also Like: Mortgage Broker vs Realtor

Why Work with a Mortgage Broker?

These programs can be tricky to figure out on your own. A good mortgage broker like AJP Mortgage knows the rules, helps prepare your application, and negotiates to get you the best no down payment mortgage in Ontario.

Why Some Buyers Prefer No Down Payment Options?

Opting for a no down payment option for residential mortgage Ontario, appeals to many buyers for various reasons. Here’s a comparison showing the key differences between no-down-payment, low-down-payment, and standard-down-payment options. Each has its advantages and potential costs:

| Feature | No Down Payment Option | Low Down Payment (5-10%) | Standard Down Payment (20%) |

| Initial Cash Outlay | Lowest | Moderate | Highest |

| Monthly Mortgage Payments | Higher | Moderate | Lower |

| Mortgage Insurance Costs | ✔ Yes | ✔ Yes | ❌ No |

| Time to Build Equity | Longer | Moderate | Shortest |

| Cash Availability | ✔ Preserves savings | Partially preserves savings | High cash outlay |

| Eligibility Requirements | Stricter credit/income | Moderate | Most flexible |

| Investment in Other Assets | ✔ Allows flexibility | Some flexibility | Limited |

| Higher Total Loan Amount | ✔ Highest loan amount | Higher than standard | Lowest |

| Risk in Market Volatility | ✔ Higher risk | Moderate risk | Lowest risk |

Risks and Things to Know About No Down Payment Mortgages

Getting a no down payment mortgage in Ontario can help you buy a home faster. But there are some important things to keep in mind.

Higher Monthly Payments

Because you’re borrowing the full price of the home plus any extra loan for the down payment, your monthly bills will be bigger. Make sure you budget well so it doesn’t stress you out.

Mortgage Insurance Costs

If your down payment is less than 20%, you’ll have to pay mortgage insurance. This protects the lender but adds to your monthly costs. The smaller the down payment, the higher the insurance usually is.

Slower Equity Growth

Since you start with no down payment, you don’t own part of the home right away. It will take longer to build equity, which can make it harder to refinance or borrow later.

Risk of Owing More Than Your Home Is Worth

If home prices drop, you could owe more than the house is worth. This is a bigger risk with no money down mortgages since you borrowed everything.

Tougher Qualification Rules

Lenders want good credit, steady income, and low debt. You might also face higher interest rates because this kind of loan is riskier for them.

Closing Costs Still Apply

Zero down doesn’t mean zero costs. You’ll need extra cash for closing fees, land transfer taxes, inspections, and more.

Tips to Make It Work

Check your credit and try to improve it.

Save a little emergency money for surprises.

Work with a trusted mortgage broker like AJP Mortgage who knows how to get these loans safely.

Read all the rules before you sign anything.

Knowing these things helps you avoid surprises. With a good plan, a no down payment mortgage can help you buy your home sooner and with less stress.

Frequently Asked Questions About No Down Payment Mortgages

What is a no down payment mortgage?

It’s a home loan that lets you buy a house without paying any money upfront. You get the mortgage without needing cash for a down payment, often through special programs or government help.

How can I qualify for a zero down payment mortgage in Ontario?

You usually need good credit, steady income, and low debt. If your down payment is borrowed or gifted, you’ll have to prove where it came from. A mortgage broker can help you find lenders that offer these loans and boost your chances.

Are there really programs to buy a house with no down payment?

Yes! Programs like the First-Time Home Buyer Incentive, the Home Buyers’ Plan, rent-to-own options, and some lender programs make it possible to buy without a down payment in Ontario.

What are the risks of a no money down mortgage?

You might have higher monthly payments, pay mortgage insurance, build equity slower, and if home prices fall, you could owe more than your home is worth. It’s important to think these through before you decide.

Can I get a no down payment mortgage with bad credit?

Most lenders want good credit for these loans. If your credit is low, try to improve it first, or consider saving a small down payment and talk to a mortgage broker for advice.

Is rent-to-own a good no down payment option in Ontario?

Rent-to-own can help if you don’t have a down payment saved yet. Part of your rent goes toward buying the home later. It’s a flexible option, but make sure to read the terms carefully.

How much are closing costs with a no down payment mortgage?

Closing costs usually run from 1.5 to 4 percent of the home price. These include legal fees, land transfer tax, inspections, and other fees. These costs are not covered by zero down mortgages.

Can I combine no down payment mortgage programs?

Yes! You can mix programs like the Home Buyers’ Plan with the First-Time Home Buyer Incentive to lower the cash you need upfront. A mortgage broker can help you find the best combo for you.

How AJP Mortgage Can Help You Get a No Down Payment Mortgage in Ontario?

Buying a home without a big down payment can feel tricky, but you don’t have to do it alone. At AJP Mortgage, we’re here to help you find the best way to get a no down payment mortgage Ontario that fits your situation.

Why Work with AJP Mortgage?

Wondering why AJP Mortgage could be the right partner for your home journey? Here’s what sets us apart.

We Know the Programs

From the First-Time Home Buyer Incentive to the Home Buyers’ Plan and zero down mortgage options in Ontario, we know what’s available. We’ll explain each one in simple terms and help you see which option fits your situation best.

Personal Help

Everyone’s finances are different, and we get that. We listen, understand your goals, and guide you to the no money down mortgage that works for you. You will not feel lost or overwhelmed along the way.

Clear and Honest

We tell it like it is. You will know what to expect, including any costs or risks, so you can make smart choices without surprises.

We Handle the Details

Paperwork, lender calls, approvals. We take care of it all so you can focus on getting ready to move in and enjoy your new home while we handle the hard stuff.

Real Stories from People Like You

Discover how everyday people just like you overcame challenges, found the right mortgage, and made their dream of owning a home a reality.

Sarah’s Story

Sarah wanted to buy her first home but didn’t have a down payment. We helped her use a government program to cover part of it. Now, she’s happily living in her own home and feeling confident about the future.

Robert’s Story

Robert had good credit but no savings for a down payment. We found a zero down mortgage that worked for him and guided him through the process. He moved in quickly without stress and is enjoying his new home.

Priya’s Story

Priya thought owning a home was impossible. We showed her no down payment options and helped her every step of the way. Today, she’s enjoying the freedom and pride of having her own home.

Ready to Take the Next Step?

Buying a home with no down payment in Ontario may feel overwhelming, but it doesn’t have to be. At AJP Mortgage, we make it simple and personal. We’ll explain how no down payment mortgages work, who qualifies, and what each option could mean for your monthly payments.

We’ll help you compare different lenders, find the best rates, and guide you through the application step by step so there are no surprises. Our goal is to make homeownership possible sooner and easier than you might expect.

Reach out today, and let’s explore the right plan for you so you can take that exciting step toward owning your home with confidence.